David Andolfatto serves as a Senior Vice President in the Research Division at the Federal Reserve Bank of St. Louis. He is Canadian-born to Italian immigrants and worked in the construction sector before going to school to become an economist. He worked in the Canadian university system for 20 years before joining the Federal Reserve. He joined the Fed in 2009 and advises St. Louis Fed President James Bullard on monetary policy. Mr. Andolfatto also coordinates FOMC briefings and participates in Research Division matters with colleagues.

Interview Date : 2nd February 2021

- David Andolfatto (All Interviews)

- When did you learn about Bitcoin?

- Monetary theorists

- What is the best use-case for that model?

- What kind of a threat are Cryptocurrencies and Bitcoin?

- Does the Bank need to get in touch with the crypto space?

- Can the cryptosystem beat the banking system?

- Do you think the banking infrastructure has to be reconstructed?

- Is Bitcoin a new revolution?

- What do you think of major corporations investing in Bitcoin?

- What do you think about the argument that the dollar is used for financing terrorism?

- Is the government inflating people’s wealth away?

- What is the M2 graph display?

- Does the M2 graph show the amount of printed money?

- How does the M2 money supply increase?

- Is inflation currently happening?

- Could Bitcoin be good for diversifying one’s portfolio?

- Would Bitcoin make a good currency system?

David Andolfatto (All Interviews)

When did you learn about Bitcoin?

I first started looking into Bitcoin around 2013. My initial reaction, like many economists, was one of skepticism. But once I looked under the hood, I recognized something very familiar and interesting. The basic problem that Bitcoin was trying to solve was in managing a virtual database of transaction histories without the aid of a delegated intermediary. The basic idea is centered on the notion of a decentralized consensus-based record-keeping system.

Monetary theorists

Monetary theorists have for a long time talked about social credit systems, where people organize an activity with the aid of a “virtual shared ledger” that records each member’s contribution to society. This virtual ledger, I noted, was maintained by the community, and not by any delegated third party. This is the similarity I noted with the consensus-based recordkeeping system in Bitcoin. Bitcoin is very much like a social credit system. What has happened is that innovations in data storage, communication, and cryptography have permitted this form of consensus-based record-keeping system to scale. This idea intrigued me early on.

What is the best use-case for that model?

Early on, I thought one of the nice use-cases was international remittances. The plumbing of the banking system is still pretty archaic, but there has been a lot of progress made over the years. It is surprising how the banks within the country still don’t really communicate with each other as well as they should. It’s even worse for cross-border communications. For example, if you want to send money from a St. Louis bank to Russia, it could take days. It shouldn’t take that long. It should be more like the way Paypal works.

What kind of a threat are Cryptocurrencies and Bitcoin?

Bitcoin and cryptocurrencies pose the threat of competition for fiat currency systems, intermediaries, and central banks. We should keep in mind, however, that currency competition has always been part of the landscape, and we’ve always had local currencies, like the Ithaca hour. The threat is more pronounced in mismanaged economies. Traditionally, people would seek alternatives to the local currency, like the U.S. dollar. But acquiring and keeping dollar bills safe is costly. People wouldn’t normally have access to a U.S. bank account. But now with the Internet, people with phones can just download an app, and they will have access to this alternative competing monetary system. I think this is potentially good in the sense that it could provide a competitive threat and so serve as a disciplining device for governments, banks, and money processors. This competitive threat can be healthy, and this could be one of the main benefits of Bitcoin and cryptocurrencies.

Does the Bank need to get in touch with the crypto space?

Banks don’t need to enter the crypto space narrowly defined. Bitcoin, for example, is inherently inefficient to transfer value. It may seem more efficient than the existing banking infrastructure, but this is because the banking system design is not optimized. We could fix that design and use very conventional database management systems to affect value transfers using a central ledger operated by a trusted third party. Banks and other intermediaries will innovate along this dimension and potentially offer systems that are inspired by “blockchain,” even if they are not really blockchain-based protocols.

Can the cryptosystem beat the banking system?

If you can trust a third party, then there is nothing that beats it. The question is whether or not you trust your accountant. For the accountant to credit and debit accounts, it’s very simple. Banks are models of trusted third parties and are going to leverage their reputation stating they don’t need to rely on things like proof-of-work. Why should they? You are basically asking a community of people you don’t know to play a non-cooperative game against each other to help you manage your books. This is the price one has to pay for bypassing conventional intermediaries. It may be a price worth paying for some. But it won’t be for most people, I don’t think.

Do you think the banking infrastructure has to be reconstructed?

I think it is something to be fixed. The system in Europe is probably one of the most advanced ones in the sense that they have zero fees at the user end and a good internet banking system. The United States was an international payment settlement leader in the 1970s. They produced ACH, the Automated Clearing House payment, which for a long time took 2 to 3 business days to clear payments, albeit in a very cheap way. That 1970s infrastructure is still in place in the United States. Many countries, including some countries in Africa, have been able to leap from this system, and the United States is slowly catching up. Also, people like myself and others have been advocating for a central bank digital currency that will have a zero user-fee, free access, and fully insured accounts with real-time gross settlements.

Is Bitcoin a new revolution?

A lot of young people think this FinTech is very revolutionary, but this revolution is just a part of an ongoing evolution in database management systems. When I first went to Italy with my mother in 1971, I was 10 years old. I remember before we went on this trip from Vancouver to Italy, we had to get a telephone book and look for Thomas Cook or American Express (offices). We needed to obtain a traveler’s cheque to be able to exchange Canadian dollars for Italian Lira. We were told that we would need a traveler’s cheque to take with us to a corresponding bank in Italy for currency exchange. Traveler’s cheques alone took 2-3 weeks to be issued and were quite costly. When we flew to Italy, my uncle took us 50 km to the nearest bank that would process the cheque to conduct the currency exchange. Fast forward, right before the COVID-19 pandemic hit, I would fly anywhere with my credit card and didn’t have to think about anything in terms of arranging for methods of payment. The lesson of this story is that there has been a tremendous amount of innovation in payment settlements before cryptocurrencies.

What do you think of major corporations investing in Bitcoin?

It’s up to them to invest where they want. Investors will have to ask what they’re investing in when they buy Tesla shares. The same is true for when investors buy into a car company, a crypto investment fund, etc.

What do you think about the argument that the dollar is used for financing terrorism?

I don’t think you can do very much about this, to be honest. It’s not like terrorism didn’t exist before the dollar.

Is the government inflating people’s wealth away?

In the U.S., inflation since the 1980s has averaged close to 2% per annum. If you are someone who held all your wealth in the form of cash, you would have seen a significant decline in your wealth over the years. But most people do not hold most of their wealth in the form of cash. And non-cash assets and securities tend to have rates of return that adjust with inflation.

What we have to be on guard for is sudden changes in the inflation rate, up or down. This is one of the main jobs of the central bank: to keep inflation low and stable. This is precisely why I say that while Bitcoin may make for a good long-run store of value, it makes for lousy money where the stability of the short-run rate of return is more important.

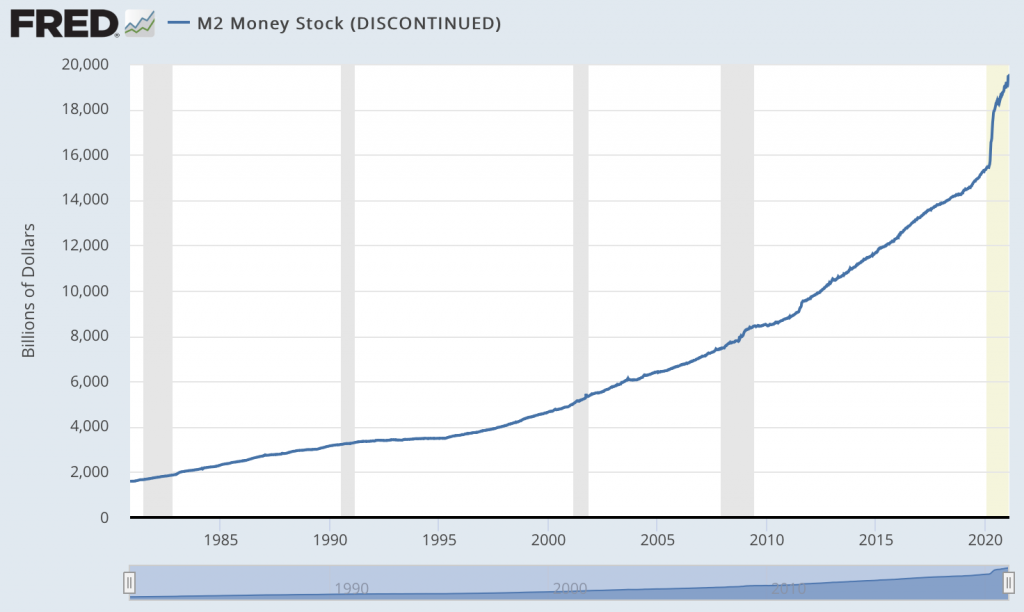

What is the M2 graph display?

M2 is a measure of a money supply. There is no unique definition of money, so economists have come up with a number of different definitions.

The next major part of the money supply is your checking accounts. So, when banks create loans, they also create deposit accounts that are redeemable on demand. So, if you count the checking accounts plus currency, it’s called M1. M2 is a bit broader than M1 because it also adds saving accounts. Looking at the M2 graph, you are seeing the money supply that is available to Americans and also people who have American checking accounts. That’s the money supply measure that’s plotted in the graph.

Does the M2 graph show the amount of printed money?

The M2 graph does not show you the money printed. Printing usually refers to paper bills. The bills in existence are not controlled by the government or by banks. The paper bills get into circulation where you go to a bank and withdraw them from your account. So, what you see here is not printing but banks issuing deposit liabilities to their customers rather than viewing this as money supply.

How does the M2 money supply increase?

In 1980, the federal government changed its monetary policy regime to an interest rate policy regime. Thus, the M2 graph mainly reflects the demand for money – not the money supply. What you see at the end of the graph is a sharp spike up in the demand for money. That spike displays all the firms that conducted withdrawals on their credit lines from their banks when the coronavirus broke in early 2020. If a company requests a credit to their deposit account with a million dollars, the company all of a sudden will have a million dollars in their savings account. And, our data picks it up due to the demand for money. The banks created the money that people and firms demanded. The other thing that’s contributing to the spike is that the government is printing a lot of debt to overcome this pandemic. These two factors account for most of that increase.

Recall that the Fed also lowered the interest rates pretty close to 0. Now, the interest rates for competing for safe securities are considerably lower than what it was prior to the crisis, thus the opportunity cost of holding money in a checking account isn’t so great.

Is inflation currently happening?

We haven’t seen inflation, at least not yet. Some people complain that the government statistics are bogus. But the privately-operated Billion Prices Project shows inflation that is consistent with government measures. Whether inflation becomes a problem in the future, we’ll have to wait and see. Certainly, the forecast is for a transitory increase in the rate of inflation as the economy re-opens from the pandemic.

Could Bitcoin be good for diversifying one’s portfolio?

Bitcoin could potentially be a good store of value for people who want to diversify their investment portfolio a little. I don’t think Bitcoin is going away any time soon. Historically, there have always been competing local currencies that would serve the local constituency, but in today’s modern age, a social network or locality is no longer constrained by physical proximity. Bitcoin serves a constituency for people who value the permissionless aspect and don’t trust the government. Bitcoin isn’t the only cryptocurrency out there, and there are many more variances designed in a way that serves their niche markets – their niche constituency.

Would Bitcoin make a good currency system?

I do not think so–please see my blog post on why gold and bitcoin are lousy money systems.

Interviewer , Editor : Lina Kamada

【Disclaimer】

The Article published on this our Homepage are only for the purpose of providing information. This is not intended as a solicitation for cryptocurrency trading. Also, this article is the author’s personal opinions, and this does not represent opinion for the Company BTCBOX co.,Ltd.